One of the tools our financial planners use in consult with their clients is a simple concept called Know Your Ratio.

Understanding this ratio can allow you to self-diagnose your financial health in less than 15 minutes, telling you if you’re on the path toward financial freedom.

This is a tool used to evaluate, track and hold CWA clients accountable toward their wealth accumulation goals by ensuring they are not overspending today, under saving for tomorrow, or falling short on tax payments. This benchmark is a simple and realistic view of ideal spending, and a reminder of where your money should be positioned to ensure you can live both comfortably today, and into tomorrow.

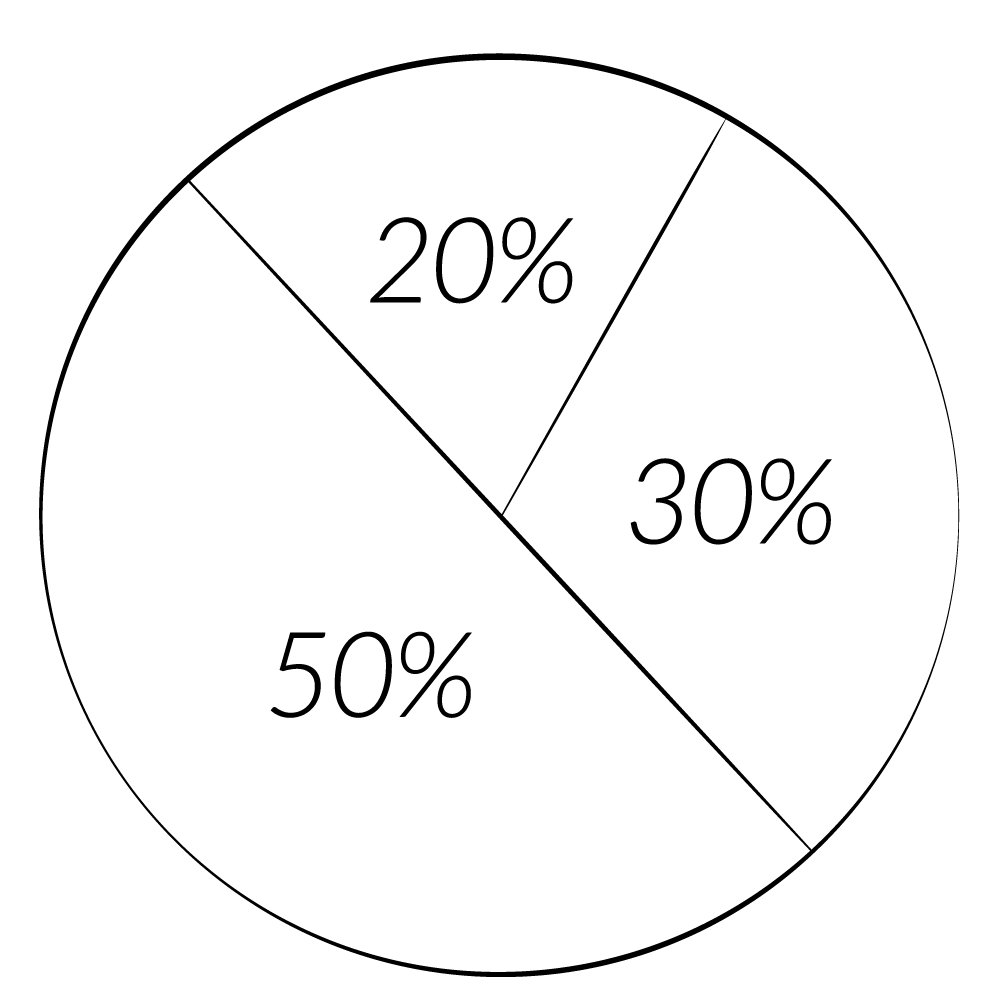

Simply stated, the 50/30/20 Rule evaluates the three main categories of where your money goes. Each of the three numbers are a percentage of your total net income.

– 50 percent: represents the amount of your lifestyle spending and debt payments

– 30 percent: represents the amount you pay in taxes including federal, state and payroll taxes

– 20 percent: represents your savings, including retirement savings as well as personal and college savings

Think about it

Too often people make the mistake of starting an exercise like this by focusing on the largest piece first: personal spending and debt payments.

It is a mistake to start with the 50% category first because it is the most difficult category to define and track accurately. How many times have you started or revised a personal budget? Do you like tracking your monthly spending? Most people do not.

A majority of the budgets that CWA financial planners see are off by at least 20-25%. People are terrible at estimating how much money they spend, and are even worse at holding themselves accountable when it comes to sticking to that spending goal.

This old way of budgeting, tracking and then saving what is left over is about as successful as a New Year’s diet resolution. There is a better way—more importantly, you don’t have to fool yourself or waste time tracking how many pumpkin spice lattes you had this month.

Step 1: Capture and define your net income

Asking a dentist how much money they make is not an easy question. Here is a hint: take a look at your December 2017 profit and loss statement for your practice. Take your net collections and subtract direct costs (staff salaries, payroll taxes, dental and office supplies as well as any lab or implant costs) and your fixed costs. The result is your net income before pension funding, salary (including spouse salary), perks or any debt, depreciation or interest expense. Use this number, write it down.

Step 2: Calculate your personal ratios

![]()

Let’s start with the smallest ratio, the savings component. Gather your year-end 2017 pension reports and investment statements. Add up your total contributions to your pension plans (do not count the staff cost portion), IRAs and any after-tax personal savings that you did in 2017. Write down what you saved in 2017.

Next, look at the 30% category which covers taxes. Find your 2017 personal tax returns and W-2’s to capture your total federal, state and payroll taxes paid. When capturing your payroll taxes, make sure that you are picking up both the employer and the employee portion of payroll taxes for your salary and your spouse’s salary. Record this number in total.

Finally, we can look at the 50% category which consists of personal spending and debt payments. Take your net income, subtract what you saved and what you paid in for taxes and the rest goes into this category. Simply put, if you didn’t save it or send it to the IRS then you spent it on something.

Step 3: Analyze your numbers

The next part of this exercise is to analyze the results. To illustrate the application let’s use the data from a recent meeting with a long-term client. His practice net income in 2017 was $400,000. We started his review session by looking at their total savings in 2017:

– Salary deferrals = $18,000

– Spouse salary deferrals = $18,000

– Employer contribution = $35,000

– Roth IRA funding = $5,500

– Spouse Roth IRA funding = $5,500

This was total savings of $82,000 or 20.5% of their $400,000 net income.

This quick calculation immediately told us the clients’ savings component of their financial plan was on track. Because they were saving into the tax-deferred and tax-free environments, their financial planner could assume their tax planning was also going to fit in the 30% category.

After this quick exercise the team was able to confirm that the big picture of their financial plan was in-line and on-track. The client had financial peace of mind knowing that they were in balance. That allowed us to spend the rest of the day diving into specific questions, concerns and goal setting for both their practice and personal lives.

What if I’m not in balance?

Many times, especially when meeting with new clients, we will find that the ratios aren’t lined up to the 50/30/20 goal. When this happens, the data points you to the area that you need to focus on first.

Clients usually struggle with a lower savings ratio, which presents many problems. When the savings ratio is low, more than likely personal spending and debt ratio is too high. But that’s not all.

Let’s think about the client with a total net income on $400,000. If they were only saving 5% of their income into a brokerage account, which doesn’t have the same tax advantages, then their ratio would look something like this:

– 61% or $245,000 in spending and debt service

– 34% or $135,000 in taxes paid

– 5% or $20,000 in savings

At 5% they obviously aren’t saving enough for retirement, but this situation leads to an even bigger issue. The client in that case would also be used to a more expensive lifestyle. Because most of us want to retire with the same standard of living we have during our careers, they are in desperate need of saving more than even the 20 percent ratio to keep up with themselves in retirement. All the while, they are paying the IRS more than they have to—if this is not reversed, this client would never reach financial freedom.

What’s your ratio?

The best thing about the 50/30/20 ratio is that it works on every client no matter your net income level. I’ve had clients that net over $1 million a year, and with proper tax planning, are able to keep their taxes at or under 30% of their total net income. The same ratio works just as well at the lower income levels, as these earners will have a lower marginal federal tax rate, yet their payroll taxes as a percentage of their total income will be much higher.

I’ve even used the 50/30/20 ratio with some of my client’s adult children. If you can educate your adult children on this concept at an early age and maintain it as their careers progress, you will have given them the gift of long-term financial independence.

What’s your ratio?

At CWA, when we meet clients with a low savings ratio, we approach the conversation educationally. Simply understanding the philosophy of the 50/30/20 Rule can help them identify their problem. Perhaps the problem is as simple as saving into the wrong environment. Or, perhaps the client is making poor choices with respect to paying down or paying off personal and practice debt too aggressively. Other times, we may need to make hard choices with respect to personal spending decisions.

We know it’s hard. Let our professionals help you reach your goals.

{kind=link}